A senior White Home official has accused main banking commerce leaders of refusing to affix earlier talks on stablecoin rewards, escalating a dispute that has grow to be one of many last stress factors forward of the Senate Banking Committee taking over the CLARITY Act this week.

In a Might 11 put up on the social media platform X, Patrick Witt, govt director of the White Home Presidential Advisory Committee on Digital Property, stated he had requested American Bankers Affiliation President Rob Nichols and different financial institution commerce CEOs to attend the February conferences geared toward resolving the query of stablecoin rewards and yield.

He acknowledged:

“I particularly requested the attendance of Mr. Nichols and different financial institution commerce CEOs on the conferences we hosted again in February to resolve the stablecoin rewards/yield challenge. They refused. I assume the White Home was beneath them?”

The criticism injected the White Home extra straight right into a combat that has divided banks, crypto firms, and lawmakers forward of a scheduled Might 14 markup of the CLARITY Act.

The invoice is designed to create a broader market construction framework for digital belongings, however the therapy of stablecoin rewards has grow to be a flashpoint over competitors for deposits, shopper yield, and the long run form of dollar-based funds.

Witt’s feedback additionally reframed the timing of the banking business’s objections. Relatively than a brand new technical concern rising earlier than a committee vote, the White Home official solid the dispute as an unresolved challenge that banking leaders had a possibility to handle months earlier.

Banks reopen stablecoin rewards combat earlier than markup

Over the weekend, the American Bankers Affiliation (ABA) urged financial institution executives and workers to press senators for tighter restrictions within the CLARITY Act earlier than the committee vote, warning that the present invoice may nonetheless permit crypto corporations to supply reward constructions that resemble curiosity on deposit-like merchandise.

Nichols advised bankers that lawmakers wanted to listen to from the business earlier than the laws superior.

The ABA’s concern is that stablecoin issuers, exchanges, or associated firms may entice buyer funds by providing returns on belongings that compete straight with conventional financial institution deposits.

That argument has grow to be central to the US financial institution foyer’s marketing campaign.

Banks depend on deposits as a funding base for loans to households, small companies, farms, and firms. If clients transfer money into stablecoins that supply rewards, banks argue that lenders may face increased funding prices, tighter margins, and fewer capability to increase credit score.

The banking business has described the present compromise language as leaving a loophole.

In its view, a ban on stablecoin issuers paying yield could be inadequate if affiliated exchanges, brokers, or different crypto platforms may ship comparable financial advantages by way of rewards, rebates, or incentive applications.

That place has put banks at odds with crypto firms that see the rewards language as a fundamental competitors challenge.

Stablecoin reserves are usually held in money, short-term Treasuries, or different liquid devices that generate earnings. The coverage combat facilities on whether or not customers ought to have the ability to obtain a part of that return, and which kind of establishment needs to be allowed to supply it.

The latest Senate compromise has tried to separate passive yield from activity-based rewards.

That distinction was meant to forestall stablecoins from turning into direct substitutes for interest-bearing deposits whereas preserving room for crypto platforms to reward customers for participation, funds, or different providers.

White Home evaluation undercuts the lending warning

The banking business’s warnings have met resistance from the White Home’s personal financial evaluation.

The Council of Financial Advisers stated in an April report that banning stablecoin yield would offer solely a marginal raise to financial institution lending underneath its baseline assumptions. The CEA estimated that such a ban would improve financial institution lending by about $2.1 billion, equal to roughly 0.02% of whole lending within the base case.

That discovering provides the administration a counterweight to the banking sector’s declare that stablecoin rewards may meaningfully harm credit score creation.

The report argued that almost all stablecoin reserves wouldn’t be completely faraway from the banking system. As an alternative, reserves held in money, financial institution deposits, or Treasury devices would proceed to flow into by way of monetary markets in numerous types.

The CEA additionally stated a extra extreme influence would require a a lot bigger stablecoin market and extra restrictive assumptions about how reserves are held. Within the administration’s framing, stablecoin rewards could have an effect on financial institution margins, however the baseline impact on lending capability seems restricted.

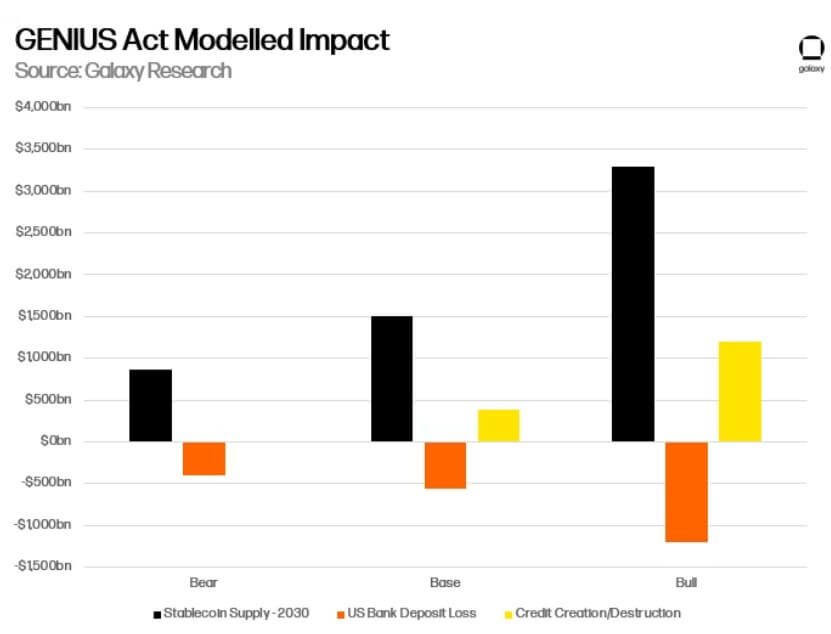

Furthermore, a separate evaluation by Galaxy Analysis furthered the argument by specializing in the worldwide circulate of {dollars}.

Galaxy stated banks had been overstating the chance that stablecoin progress would merely drain home deposits. Its mannequin projected that a lot of the expansion underneath a regulated stablecoin framework would come from offshore customers in search of simpler entry to dollar-denominated belongings.

That discovering modifications the financial lens. If stablecoins principally draw funds from US financial institution accounts, banks face a direct deposit migration drawback.

Nonetheless, if a lot of the expansion comes from overseas customers shifting into greenback stablecoins, the impact may very well be an influx into US monetary infrastructure moderately than a one-way drain from home lenders.

Galaxy estimated that 60% to 70% of stablecoin progress underneath the GENIUS Act framework may originate offshore. It additionally projected that imported deposits from overseas demand may exceed home deposit migration by roughly 2:1.

The agency stated every newly minted stablecoin greenback may generate about 32 cents of internet US credit score, with whole credit score enlargement reaching about $400 billion by way of 2030 in its base case and as a lot as $1.2 trillion in a stronger progress state of affairs.

It additionally projected that stablecoin reserve demand may compress Treasury invoice yields by 3 to five foundation factors, probably reducing federal borrowing prices.

In the meantime, Galaxy didn’t dismiss the stress on banks. The report stated some low-cost deposits would seemingly migrate, funding prices may rise on the margin, and internet curiosity margins may compress in enterprise traces delicate to charge competitors.

Nonetheless, the agency concluded that stablecoins may stress banks that depend on low-cost deposits, improve demand for US Treasury payments, import offshore greenback capital, and increase the attain of the US monetary system.

Crypto allies accuse banks of defending margins

Crypto advocacy teams have seized on the ABA’s push as proof that banks try to dam competitors days earlier than the committee vote on the CLARITY Act.

Coinbase-backed Stand With Crypto urged supporters to contact senators, saying banking lobbyists had been attempting to weaken stablecoin rewards language earlier than the markup.

The group framed the dispute as a consumer-rights challenge, arguing that customers ought to have the ability to earn returns on their very own digital belongings moderately than have that worth captured by intermediaries.

Cody Carbone, CEO of The Digital Chamber, stated banks had months to barter over the difficulty and had been now attempting to drive modifications late within the course of. He described the ABA marketing campaign as an try to protect incumbents from competitors after earlier alternatives to have interaction had handed.

Sen. Bernie Moreno, an Ohio Republican on the Banking Committee and a supporter of crypto laws, used sharper language in regards to the financial institution’s opposition to CLARITY Act.

He accused the “banking cartel” of attempting to protect a system during which banks pay depositors short time incomes earnings from lending and securities portfolios.

Moreno wrote on X:

“In the course of the Biden period, these similar banks labored hand-in-glove with Sen. Warren and her allies to debank People, together with President Trump’s family. They shut down accounts of conservatives, patriots, and anybody who dared problem the regime, all whereas regulators utilized stress underneath schemes like Operation Choke Level 2.0. It wasn’t about threat. It was about political management. Now that progressive stablecoins threaten to interrupt their monopoly and provide you with precise monetary freedom? They’re operating to Congress once more, screaming about ‘threats to financial progress and monetary stability.’”

Moreno’s assertion confirmed how the stablecoin rewards dispute has moved past technical drafting.

The combat now carries a broader political message about monetary competitors, shopper returns, and resentment towards massive banking establishments.

That rhetoric may assist crypto advocates rally assist, particularly amongst Republicans who view stablecoins as a part of a broader agenda round monetary innovation and greenback competitiveness.

Nonetheless, it additionally dangers hardening opposition from lawmakers who’re already involved that crypto corporations are in search of bank-like privileges with out equal oversight.

Markup will check whether or not the stablecoin compromise can maintain

The Senate Banking Committee’s Might 14 markup will present whether or not the rewards compromise can stand up to a coordinated pushback from the banking business.

If the committee advances the CLARITY Act with the present language largely intact, crypto corporations will declare momentum, and banks will seemingly shift their marketing campaign to the total Senate.

If lawmakers tighten the rewards provisions, the banking business could have succeeded in reopening one of the crucial contested components of the invoice on the last stage earlier than markup.

In the meantime, the vote may even check the broader coalition behind the CLARITY Act. Republicans have pushed digital-asset laws as a precedence, whereas some Democrats have remained open to a market-structure invoice if it consists of stronger shopper protections, ethics, and anti-money-laundering provisions.

The stablecoin combat complicates that effort as a result of it cuts throughout a number of coverage traces directly. It raises questions on financial institution funding, shopper yield, Treasury demand, offshore greenback utilization, and the function of crypto corporations in funds.

That offers senators a number of causes to demand modifications, but in addition makes the difficulty troublesome to settle cleanly.

{kind=link}